We offer an array of retirement & profit sharing plans that match your needs and business. Schedule a Free Consultation Today.

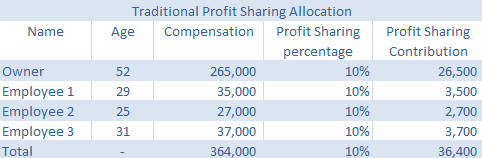

In traditional profit-sharing plans, all participants receive an equal profit-sharing allocation.

Advantage

Mandatory IRS testing may not be required.

Disdvantage

The plan allocation cannot be skewed in favour of the owners or key employees. This is a major disadvantage if you are looking to put aside more money for yourself as the owner of the business.

Who favors this design

A business where every employee contributes the same amount of expertise in the running of the business would favour this design. For example, a small consulting firm operating in a niche segment with three employees would favour such a design.

Allocation in a traditional profit-sharing plan

| Allocation to Owner: $26,500 Allocation to Employees: $9,900 |

|---|

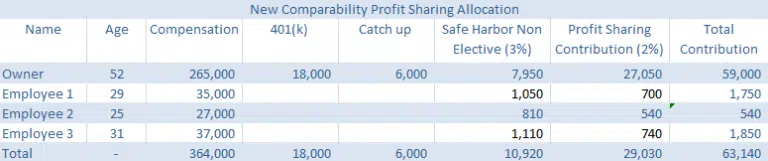

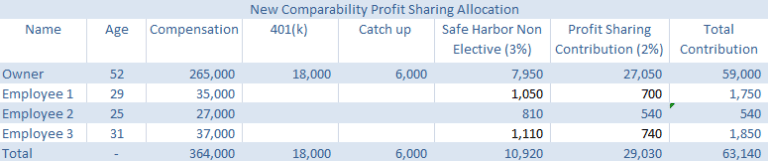

The new comparability design was born out of the need to allocate higher benefits to key employees and owners of the business.

Advantage

The business owners can contribute up to the maximum permitted amounts each year. This amount is limited by the IRS and is $61,000 for 2022(these limits are adjusted annually, so please check the IRS website).

Disdvantage

Mandatory IRS testing is required.

Who favors this design

Most firms would favor this design where employees can be segmented into different classes with each subset contributing different levels of expertise in the operations of the business. If the above example, were to be redesigned as a new comparability profit-sharing plan below is how the allocations would be made

| Allocation to Owner: $54,000 Allocation to Employees: $4,950 |

|---|

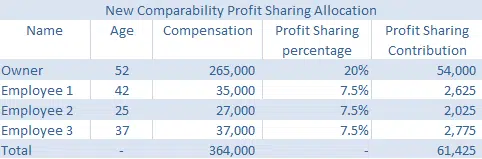

New comparability plans are dependent on the age and compensation of the employees. As such, employees with higher compensations would receive a larger amount as a contribution. Similarly, an older group of employees would end up skewing the contributions on the higher end. Below is how the allocation would look if two of the employees were older.

| Allocation to Owner: $54,000 Allocation to Employees: $7,425. |

|---|